Money has a strange, quiet way of weaving itself into almost every corner of the human experience. It is the invisible current that influences where we plant our roots, how gracefully we weather life’s sudden storms, the quiet choices we make every morning, and the wild dreams we dare to build for our future. Yet, for so many of us, sitting down to manage our finances triggers an immediate wave of anxiety. Between the relentless sting of daily expenses, the creeping tide of inflation, lingering debts, and the heavy pressure of distant, long-term goals, it is easy to feel completely paralyzed.

THE ACCUMULATION EFFECT (OVER TIME)

[Small Habit] ---> [Repetition] ---> [The Momentum] ---> [Financial Freedom]

(Seed) (Rain) (Deep Roots) (The Great Oak)

Building wealth is significantly less about luck and entirely about our daily psychology. It is about waking up to our own behavior, understanding exactly where our resources are flowing, and letting time do the heavy lifting. The moment we stop avoiding our bank statements and start making conscious, intentional choices, we plant a seed. If you are ready to stop breathing through your teeth every time you swipe your card, reduce your mental stress, and cultivate a foundation that lasts, these human-centric money shifts will show you how to tend to your own financial garden.

1. Facing the Mirror: Embracing Your Financial Reality

As humans, we are master evolutionary escape artists when it comes to shame or discomfort. We actively avoid looking at our bank apps because we dread the cold reality waiting for us. We tap our phones against card readers, pay our minimum balances, and drift through the weeks blindly hoping everything balances out by payday. But this ostrich-like avoidance keeps us completely stuck.

The very first power move is to strip away the judgment and simply get clear on your numbers. What is actually coming in each month after taxes? What are your unyielding, non-negotiable survival costs—the rent or mortgage, the utilities, the insurance premiums? And, most crucially, where is the rest of that hard-earned cash evaporating?

+----------------------------------------+

| THE TOTAL MONTHLY INCOME |

+----------------------------------------+

|

+----------------+----------------+

| |

+-------------------------------+ +-------------------------------+

| THE FIXED ANCHORS | | THE FLUID VARIABLE LEAKS |

| (Rent, Utilities, Insurance) | | (Subscribes, Dining, Impulse)|

+-------------------------------+ +-------------------------------+

When you track your variable spending—the casual dining, the impulsive late-night online shopping, the streaming services you haven’t watched in six months—you will inevitably unearth some startling truths. You will see how tiny, daily leaks can sink a massive ship. You might realize you are spending a small fortune out of sheer habit, boredom, or stress.

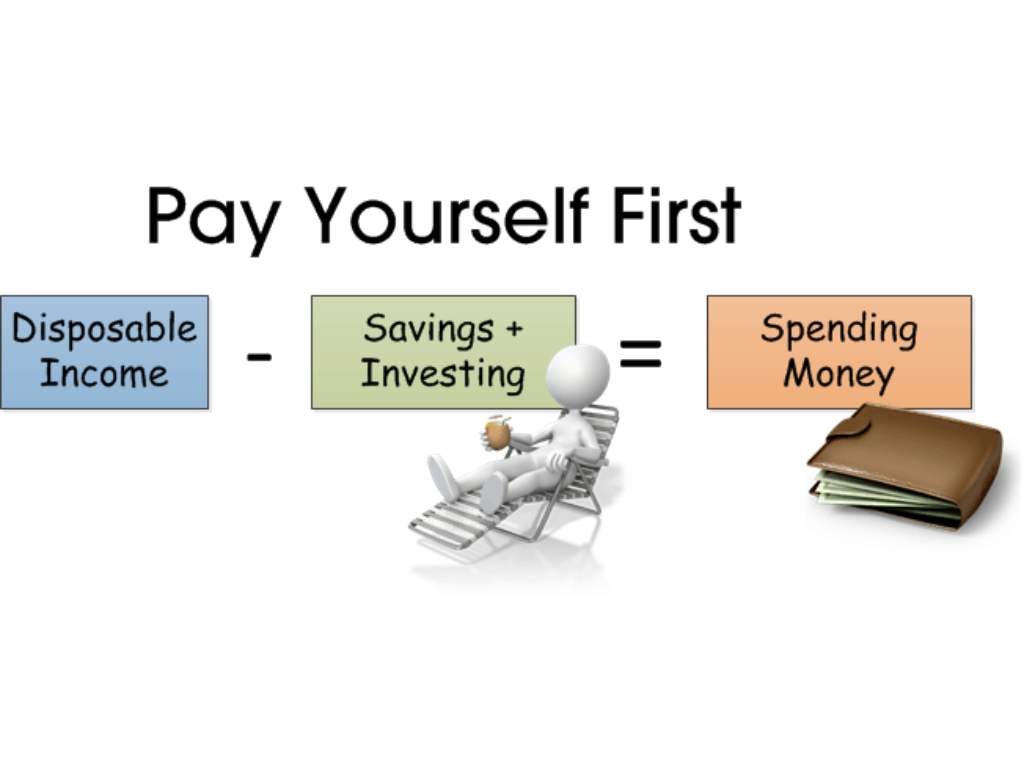

2. Pay Yourself First: Automating Your Financial Peace

If you only try to save money from whatever happens to be left over at the tail end of the month, you will almost always find an empty nest.

Our desires naturally expand to fill the space we give them. If there is money sitting casually in a checking account, our brains will subtly rationalize a way to spend it. Successful savers don’t possess a superhuman level of willpower; they simply build a system that bypasses human weakness entirely. They treat their savings as their absolute first expense, not an afterthought.

The moment your paycheck hits your account, a portion of it should immediately vanish into a separate savings or investment vehicle before your conscious mind even has a chance to play tricks on you. By automating this process, you remove the friction of decision-making.

THE WRONG FLOW: THE WEALTH FLOW:

Income -> Spend -> Save? (Usually $0) Income -> AUTOMATED SAVE -> Spend Comfortably

Even if you can only afford to send twenty dollars a week into hiding right now, do it anyway. The absolute dollar amount matters far less in the beginning than the psychological neural pathway you are carving out. You are proving to yourself that your future self is a priority. Over time, that tiny stream will carve out a canyon of capital, and you will adapt to living comfortably on the remainder.

3. The Emergency Cushion: Erecting Your Financial Umbrella

Your car’s transmission will eventually falter. A tooth will crack. An appliance will burn out, or an unexpected corporate restructuring will leave you looking for a new job. These things aren’t anomalies; they are guaranteed milestones on the human timeline. Without an emergency fund, these inevitable bumps in the road transform into catastrophic financial crises that force us to rely on high-interest credit cards or loans.

Knowing you have three to six months of basic living expenses sitting safely in a liquid, boring high-yield savings account changes your physical posture. You walk a little taller. When a crisis inevitably arrives, it is still an emotional annoyance, but it is no longer an absolute disaster. You don’t have to panic-borrow or beg for extensions; you simply write a check and move on with your life. Security isn’t just about having numbers on a screen; it is about the profound mental clarity that comes with resilience.

4. Intentional Editing: Cutting the Fat without Killing the Joy

Let’s be entirely honest: extreme, restrictive budgeting is a miserable way to live, and it almost always fails. It is the financial equivalent of a crash diet. If you try to cut out every single ounce of joy from your life—your morning coffee, dinner with your closest friends, or the hobbies that keep you sane—you will eventually experience psychological burnout. You will snap, abandon the plan entirely, and go on a reckless spending spree.

| Spending Type | Psychological Impact | Financial Action |

| Mindless Leaks | Subscriptions you forgot, impulse buys, convenience fees. | Cancel immediately; prune ruthlessly. |

| Habitual Traps | Buying lunch daily out of laziness rather than enjoyment. | Modify; plan ahead to reclaim cash. |

| True Joy | Experiences, wellness, or things that genuinely enrich life. | Keep; budget for them intentionally. |

Look at your bank statements through this lens. Keep the things that genuinely elevate your human experience, but be utterly ruthless with the mindless leaks. Cook a few more meals at home, comparison-shop your insurance policies, and introduce a mandatory 48-hour cooling-off period before making any major non-essential purchase. When your outflows perfectly match your true personal values, saving ceases to feel like a punishment and starts feeling like an alignment.

5. Escaping the Undertow of High-Interest Debt

High-interest consumer debt, particularly credit card balances, is a financial undertow that can keep even high earners swimming frantically in place for decades.

Interest is a powerful natural force that works relentlessly in two directions. When you invest, compounding interest acts like a tailwind, pushing you forward into abundance. But when you carry high-interest debt, that same compounding force acts like a crushing headwind, quietly draining your life force to pay for past choices.

DEBT UNDERCOAT (High Interest) INVESTMENT TAILWIND (Compounding)

<- [You] <--- [Interest Drags Back] [Interest Pushes Forward] ---> [You] ->

When you are trapped in a debt cycle, an enormous slice of your monthly energy is spent paying for things that have already lost their luster. Breaking out of this trap requires an aggressive, highly focused plan. Whether you prefer the Debt Snowball method (paying off the smallest balances first for a quick psychological win) or the Debt Avalanche (targeting the highest interest rates first to save the most money), the key is to stop borrowing immediately and attack the principal balances with everything you have.

6. Expanding Your Horizon: Maximizing Your Earning Potential

While learning to manage your outgoings is absolutely foundational, we have to recognize that frugality has a mathematical ceiling. You can only cut your expenses down to zero. Your earning potential, on the other hand, is theoretically limitless.

One of the most transformative realizations you can have is that your primary wealth-building tool is your career and your mind. If you find yourself budgeting down to the penny and still struggling to make real progress, the answer isn’t to squeeze yourself harder; it is to figure out how to increase the size of the pie.

THE FRUGALITY CEILING THE EARNING HORIZON

$3,000 Income $10,000+ Income

| |

v [Max Cutting Limit] v [Infinite Room to Grow]

$1,500 Floor (Rent/Food) Skill Upside / Side Ventures

This means making a deliberate decision to invest in yourself. What high-income skills can you learn over the next year that would make you indispensable to the market? This could mean sharpening your technical capabilities, studying data analytics, learning how to sell, or mastering negotiation and emotional intelligence.

Look for opportunities for promotion, explore career pivots, take on a side venture that utilizes your specific creative gifts, or consult on the side. When you combine a disciplined, intentional lifestyle with a rising income, your wealth-building journey shifts out of first gear and accelerates down the highway.

7. Let the Earth Do the Digging: The Power of Compounding

Simply hoarding cash in a traditional bank account is not enough to secure your long-term future. Savings are meant to protect you from the short-term storms of life, but investing is what actually grows your future security. If your money sits entirely in a standard checking or savings account for decades, inflation acts like a slow, invisible rust, gradually eroding your purchasing power every single day. The numbers stay the same, but the amount of groceries those numbers can buy steadily shrinks.

FAQ’s

1. What is the best way to start saving money?

Track expenses and save consistently.

2. Why is an emergency fund important?

It protects you during unexpected expenses.

3. How can I grow wealth faster?

Save regularly and invest wisely.

4. Does debt affect wealth building?

Yes, high-interest debt slows financial growth.

5. Why are financial goals important?

They keep your money decisions focused.

- Career Craft for Students and Professionals: Complete Guide

- Powerful Money Moves to Boost Savings and Grow Wealth

- Easy DIY Crafts to Make Your Space Look Beautiful

- Trend Crafting Secrets Every Creator and Brand Should Know

- 10 Powerful Books That Can Transform Your Thinking

- 7 Easy DIY Room Hacks That Made My Space Look Expensive

0 Comments