Buying a first home is one of the most defining milestones of adult life. The prospect of owning property, building equity, and having a space to truly call your own is incredibly exciting. However, the path to homeownership is often paved with financial stress, unexpected costs, and complex bureaucratic hurdles.

In a shifting economic landscape marked by fluctuating interest rates and competitive real estate markets, preparation is everything. Many prospective buyers focus solely on browsing real estate apps and attending open houses, leaving the actual financial structuring as an afterthought. This approach can lead to severe disappointment, such as being denied a mortgage, getting locked into a high interest rate, or finding themselves “house poor”—a state where housing expenses consume so much income that there is nothing left for savings, travel, or daily living.

To transition from a renter to a homeowner smoothly and confidently, you must treat your finances like a business in the months leading up to your purchase. By executing specific strategic financial maneuvers before you ever speak to a real estate agent, you protect your bank account and position yourself as a highly attractive buyer to lenders.

1. Implement a Strict Credit Freeze on New Debts and Inquiries

The Action Plan

least six to twelve months before applying for a mortgage, put a complete halt on new credit applications. Pay off existing credit card balances in full each month to keep your credit utilization ratio below ten percent. Do not close old credit accounts, as the length of your credit history positively impacts your score. Keep your financial profile completely stagnant so lenders see a predictable, low-risk borrower.

Your credit score is the single most critical factor determining the cost of your home loan. A difference of just thirty or forty points on your credit report can translate into tens of thousands of dollars saved or lost in interest over the life of a thirty-year mortgage. Lenders use this score to assess your risk profile, and they review it multiple times throughout the underwriting process, right up until the day the loan closes.

One of the most catastrophic mistakes first-time buyers make is altering their credit profile during the home-buying journey. This includes taking out a new auto loan, opening a retail store credit card to buy furniture ahead of time, or even co-signing a loan for a family member.

Every time you apply for new credit, a hard inquiry is registered on your report, which temporarily dips your score. More importantly, taking on new debt changes your Debt-to-Income (DTI) ratio, which measures how much of your monthly gross income goes toward paying off debts. If your DTI ratio spikes because of a new car payment, the amount a bank is willing to lend you for a house will drop dramatically.

2. Supercharge Your Liquidity Beyond the Standard Down Payment

Mainstream financial advice heavily emphasizes saving for a down payment, typically aiming for twenty percent to avoid private mortgage insurance. While saving a substantial down payment is vital, focusing exclusively on that number can leave you dangerously exposed to financial vulnerability on moving day.

The down payment is merely the ticket to enter the stadium; it does not cover the rest of the game. First-time buyers are frequently blindsided by closing costs, which generally range from two percent to five percent of the total loan amount. These fees cover loan origination, home appraisals, title searches, attorney fees, and local property taxes. For a four-hundred-thousand-dollar home, closing costs alone can add an extra ten thousand to twenty thousand dollars that must be paid in cash at settlement.

Furthermore, buying a home introduces immediate, unexpected operational costs. Rental properties obscure the true cost of maintenance; when a pipe bursts or an appliance breaks in an apartment, the landlord pays for it. As a homeowner, that responsibility rests entirely on your shoulders. Moving expenses, minor immediate renovations, and furnishing a larger space also drain cash reserves rapidly.

The Action Plan

Create a multi-tiered cash reserve strategy. Your total cash goal must equal your target down payment, plus five percent for closing costs, plus a separate moving and setup fund, plus a rock-solid six-month emergency fund. Never empty your entire bank account to buy a house. If making a twenty percent down payment leaves you with zero savings, you are better off putting down ten or fifteen percent and maintaining a healthy financial buffer.

3. Conduct a Forensic Audit of Your Monthly Debt-to-Income Ratio

When a bank evaluates your mortgage application, they look closely at two metrics: the front-end DTI and the back-end DTI. The front-end ratio calculates the percentage of your gross monthly income that will go toward housing expenses (principal, interest, taxes, and insurance). The back-end ratio calculates the percentage of your income that goes toward all recurring monthly debt obligations combined, including your future mortgage, student loans, car payments, and minimum credit card payments.

Most conventional lenders prefer a back-end DTI ratio of thirty-six percent or lower, though some programs allow up to forty-five percent under strict conditions. If your existing monthly debts are high, your purchasing power for a home shrinks significantly, regardless of how much money you make.

Aggressively lowering your existing debt before applying for a loan achieves two things: it immediately increases the maximum loan amount you qualify for, and it frees up monthly cash flow, making your future mortgage payment feel far less burdensome.

The Action Plan

List all of your current debts from smallest to largest or by interest rate. Use the six months before your home search to aggressively pay down high-interest consumer debt, such as credit cards or personal loans. If you have a car loan with only a few payments left, consider paying it off entirely to eliminate that monthly line item from your credit report before the lender calculates your DTI.

4. Establish a Separate, High-Yield “House Fund” and Freeze Capital in Volatile Markets

Where you store your money while saving for a home matters just as much as how much you save. A common mistake among eager investors is keeping their down payment savings in the stock market or cryptocurrency assets, hoping to accelerate their gains right up until they buy.

While investing is excellent for long-term wealth building, the stock market is inherently volatile over short periods. If the market experiences a sudden ten or twenty percent correction right when you find your dream home, your down payment could shrink overnight, forcing you to delay your purchase or sell assets at a major loss.

Conversely, leaving your savings in a traditional checking or savings account at a brick-and-mortar bank means your money is actively losing purchasing power to inflation, as these accounts often pay negligible interest.

The Action Plan

Move your home savings out of volatile investment accounts and traditional checking accounts. Place the capital into a dedicated High-Yield Savings Account (HYSA) or short-term Certificates of Deposit (CDs) that match your home-buying timeline. These vehicles offer guaranteed safety of principal while yielding a competitive return, ensuring your money is secure, growing, and fully accessible when you are ready to write an earnest money check.

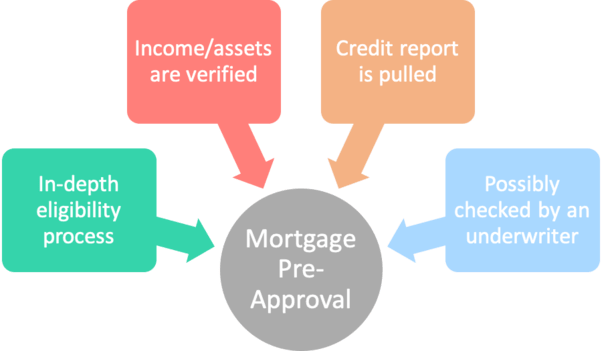

5. Secure a Verified Pre-Approval, Not Just a Pre-Qualification

In a competitive housing market, speed and credibility are your greatest assets. When you find a house you love, you must be ready to submit an offer immediately. Sellers will not take an offer seriously unless it is accompanied by proof that a financial institution will back your purchase.

Many first-time buyers confuse pre-qualification with pre-approval. A pre-qualification is a superficial estimate. You provide a lender with self-reported numbers regarding your income and debt, and they give you a ballpark figure of what you might be able to borrow. It holds virtually no weight in a serious real estate negotiation.

A pre-approval, however, is a rigorous process. The lender verifies your tax returns, W-2 statements, pay stubs, bank statements, and runs a comprehensive credit check. A pre-approval letter states that the bank has actively audited your financial background and is formally committed to lending you a specific amount of money, pending a property appraisal.

The Action Plan

Before you begin actively touring homes with a real estate agent, gather two years of tax returns, your two most recent pay stubs, and two months of bank statements. Submit these to at least two or three different lenders to compare loan terms, interest rates, and loan origination fees. Securing a formal pre-approval letter gives you a concrete budget, prevents you from looking at homes you cannot afford, and shows sellers you are a legitimate, transaction-ready buyer.

The Path to a Stress-Free Closing

The process of buying a home can feel like an emotional rollercoaster, but your financial preparation dictates whether that journey is an empowering transition or a chaotic ordeal.

By freezing new debts, building deep liquidity reserves, optimizing your debt ratios, securing your capital, and obtaining a formal pre-approval, you eliminate the guesswork from home buying. Taking these critical financial steps ensures that when you finally receive the keys to your first home, it remains a true sanctuary and a source of long-term prosperity, rather than a financial burden.

FAQs

1. How much should I save for a down payment?

Aim for at least 10%–20% of the home’s price.

2. Why is my credit score important?

A higher score can help you get better mortgage rates.

3. Should I pay off debt before buying a home?

Yes, reducing debt improves loan approval chances.

4. How much emergency savings should I have?

Ideally, keep 3–6 months of living expenses saved.

5. Why should I get pre-approved for a mortgage?

It shows your budget and strengthens your offer to sellers.

- Career Craft for Students and Professionals: Complete Guide

- Powerful Money Moves to Boost Savings and Grow Wealth

- Easy DIY Crafts to Make Your Space Look Beautiful

- Trend Crafting Secrets Every Creator and Brand Should Know

- 10 Powerful Books That Can Transform Your Thinking

- 7 Easy DIY Room Hacks That Made My Space Look Expensive

0 Comments