Money decisions shape nearly every part of life, from where you live and work to how comfortable and secure you feel about the future. Yet many people delay important financial decisions because they believe there will always be more time. The truth is that some financial moves become more difficult, expensive, or stressful when postponed for too long.

Making smart money moves does not require being wealthy, having advanced financial knowledge, or earning a large salary. Most financial success comes from building good habits, making informed decisions, and taking action before problems become bigger.

The earlier you start managing money wisely, the greater your chances of creating financial stability and reducing future stress. Whether you are just beginning your financial journey or trying to improve existing habits, these money moves can help create a stronger financial future before opportunities pass by.

Build an Emergency Fund Before You Need It

Unexpected expenses rarely arrive with warnings. Medical emergencies, job loss, car repairs, home maintenance, or family emergencies can create financial pressure almost instantly.

An emergency fund acts as a financial safety net during difficult times. Without savings, many people rely on credit cards or loans, which can create long-term debt problems.

Start by setting realistic savings goals rather than trying to build a large emergency fund immediately. Even small contributions made consistently can grow into meaningful protection over time.

The goal is not perfection. The goal is creating financial breathing room when life becomes unpredictable.

Create a Budget That Actually Works

Many people avoid budgeting because they believe it limits freedom. In reality, budgeting creates more control over money rather than less.

A practical budget helps you understand where money goes each month and identifies areas where spending can improve. The most effective budgets are simple enough to maintain consistently.

Track essential expenses, savings goals, and spending habits honestly. Avoid creating unrealistic budgets that are impossible to follow.

Budgeting is not about restricting every purchase. It is about ensuring money supports your priorities instead of disappearing without purpose.

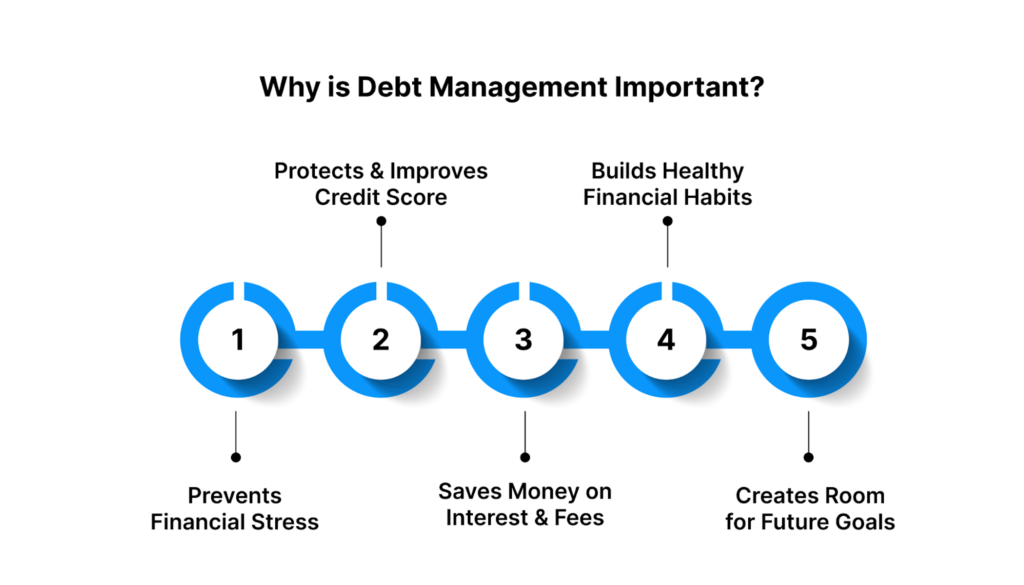

Eliminate High-Interest Debt Quickly

High-interest debt can quietly destroy financial progress. Credit card balances, personal loans, and other expensive borrowing often grow faster than expected.

Paying minimum amounts may feel manageable initially, but interest charges can significantly increase total repayment costs.

Focus on reducing debt strategically. Some people prefer paying smaller balances first for motivation, while others prioritize debts with higher interest rates.

Reducing expensive debt creates more financial flexibility and allows future income to support goals rather than past spending.

Start Investing Earlier Rather Than Later

One of the biggest financial mistakes people make is waiting too long to invest. Many assume investing requires large amounts of money or advanced knowledge.

Time often matters more than starting amounts because investments benefit from long-term growth and compounding.

Beginning with small investments can still create significant long-term benefits. Consistency generally matters more than trying to invest perfectly.

Waiting for the perfect moment frequently leads to years of missed opportunities.

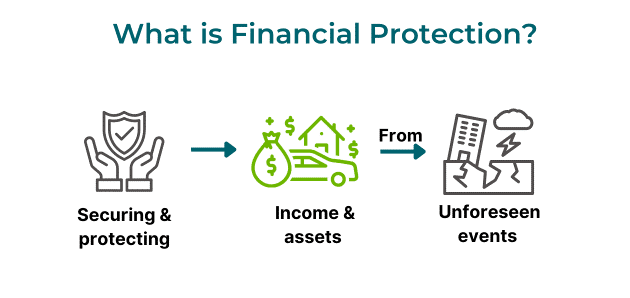

Protect Your Income and Financial Stability

Many people focus heavily on earning money but spend very little time protecting their income.

Insurance, emergency planning, and financial protection strategies help reduce risks that could create major financial setbacks.

Consider whether your current financial protections match your lifestyle and responsibilities. Losing income unexpectedly without preparation can create severe financial stress.

Protection may not feel exciting compared to investing or saving, but it often becomes valuable when unexpected events occur.

Avoid Lifestyle Inflation

As income increases, spending often increases alongside it. This pattern, known as lifestyle inflation, can prevent financial progress even when earnings improve significantly.

Higher salaries create opportunities for stronger savings, investments, and long-term security. Unfortunately, many people immediately increase expenses instead.

This does not mean avoiding enjoyment or refusing upgrades. The key is increasing lifestyle expenses thoughtfully rather than automatically.

Financial growth becomes easier when income rises faster than spending.

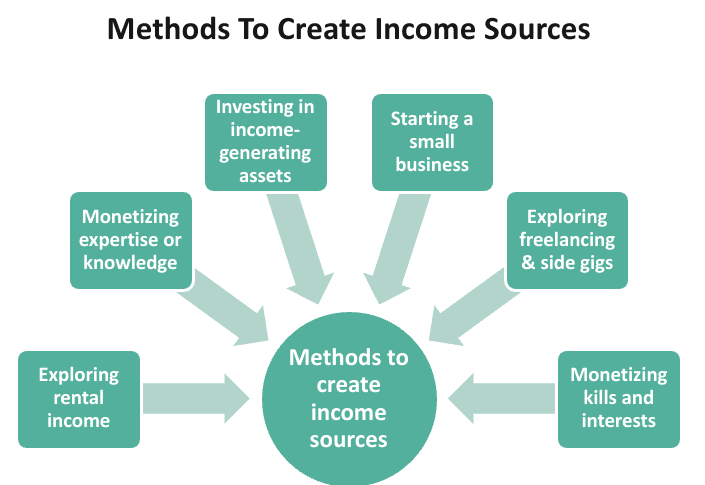

Build Multiple Income Sources

Relying entirely on one income source creates financial vulnerability. Economic changes, company restructuring, or unexpected circumstances can quickly affect earnings.

Additional income streams may include freelancing, side projects, investments, online businesses, consulting, or other opportunities.

Building extra income does not always require working significantly longer hours. Sometimes developing skills or creating scalable opportunities produces additional earnings.

Diversified income creates more financial flexibility and reduces dependence on single sources.

Improve Financial Knowledge Continuously

Financial education remains one of the most valuable long-term investments.

Understanding saving, debt management, taxes, investing, retirement planning, and financial decision-making improves money outcomes over time.

You do not need advanced financial expertise. Even learning basic concepts consistently can produce meaningful improvements.

Reading books, following reliable financial resources, and staying informed helps build confidence when making financial decisions.

The cost of poor financial knowledge often becomes expensive later.

Prepare for Retirement Early

Retirement planning often feels distant, especially for younger people. However, delaying retirement preparation can create major challenges later.

Small contributions made consistently over many years often outperform larger contributions started much later.

Retirement planning is not only about age. It is about creating financial independence and future flexibility.

Even if retirement feels far away, beginning early provides more options and reduces pressure later.

Set Clear Financial Goals

Money without direction often disappears quickly. Clear financial goals provide motivation and improve decision-making.

Goals may include purchasing a home, paying debt, building investments, traveling, starting businesses, or creating financial independence.

Break larger goals into smaller achievable milestones. Progress becomes easier when objectives feel realistic and measurable.

Goals create purpose behind financial decisions rather than relying entirely on short-term thinking.

Review Spending Habits Honestly

Many financial problems develop gradually through small spending patterns rather than single large purchases.

Subscriptions, impulse purchases, frequent convenience spending, and unnecessary expenses can quietly reduce financial progress.

Review spending periodically and ask whether purchases align with priorities.

The purpose is not eliminating enjoyment. It is understanding whether spending supports the lifestyle you actually want.

Awareness often creates improvement naturally.

Build Strong Financial Habits Instead of Seeking Quick Results

Many people search for shortcuts, fast wealth strategies, or instant financial success. Sustainable financial improvement usually comes from habits rather than dramatic changes.

Saving consistently, spending intentionally, avoiding unnecessary debt, and investing regularly may appear simple, but these habits create powerful long-term results.

Financial success rarely happens overnight.

Small actions repeated consistently often produce larger results than occasional extreme efforts.

Prepare for Major Life Changes

Life changes frequently affect finances. Marriage, children, career changes, relocation, home ownership, or aging parents can create new financial responsibilities.

Planning ahead for these transitions reduces stress and improves preparedness.

Waiting until changes arrive often limits available options and creates unnecessary pressure.

Financial preparation creates flexibility during important life transitions.

Conclusion

Money moves become more powerful when they happen early rather than late. Many people believe financial improvement requires perfect timing, large incomes, or complicated strategies. In reality, the most important step is simply starting.

Building savings, reducing debt, investing consistently, protecting income, and developing stronger financial habits create long-term advantages that become more valuable over time.

The cost of waiting is often greater than the cost of starting imperfectly.

Financial success is not determined by a single decision. It is built through many smart money moves made consistently before opportunities disappear.

FAQ’s

1. What is the first money move I should make?

Start building an emergency fund.

2. Why is early investing important?

It gives your money more time to grow.

3. How can I improve my finances quickly?

Reduce debt and track spending.

4. Should I create a budget?

Yes, budgeting helps control expenses.

5. Why are financial goals important?

They provide direction for better money decisions.

- Powerful Money Moves to Boost Savings and Grow Wealth

- Easy DIY Crafts to Make Your Space Look Beautiful

- Trend Crafting Secrets Every Creator and Brand Should Know

- 10 Powerful Books That Can Transform Your Thinking

- 7 Easy DIY Room Hacks That Made My Space Look Expensive

- The Biggest Obstacles to Personal Growth and How to Conquer Them

0 Comments