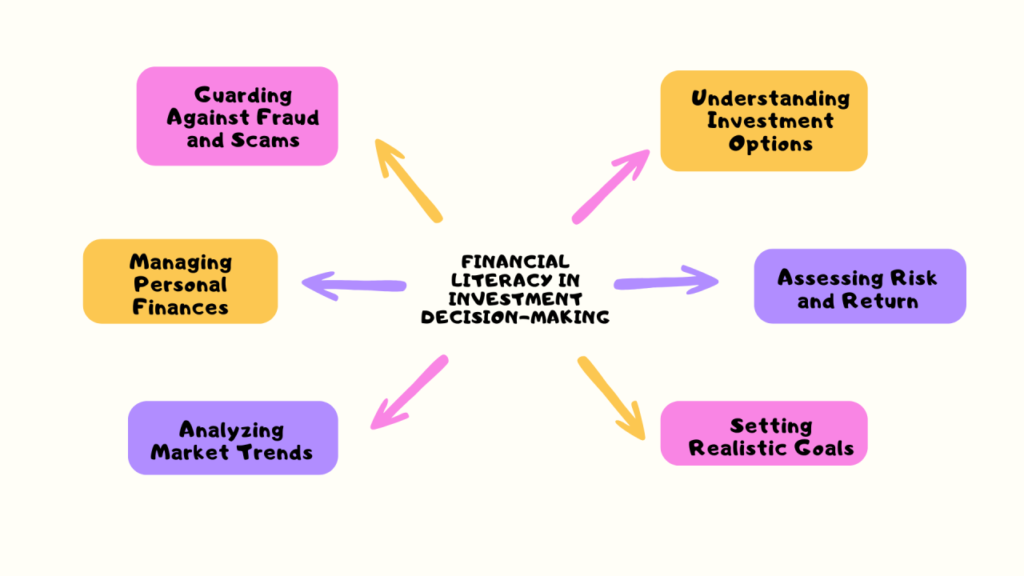

Managing personal finances is one of the most important life skills anyone can develop. Money affects almost every part of daily life, from paying bills and buying necessities to planning vacations and preparing for retirement. Yet many people struggle with financial decisions because they were never taught how to manage money properly.

Good financial habits are not about becoming rich overnight. They are about making smart decisions consistently over time. The right money moves can reduce stress, create financial security, and help people achieve their long-term goals. Whether someone is just starting their financial journey or trying to improve their current situation, understanding the basics of personal finance can make a major difference.

Here are some of the top personal finance money moves everyone should know.

Create a Realistic Budget

A budget is the foundation of strong personal finance. Without knowing where money is going each month, it becomes difficult to save, invest, or avoid unnecessary debt.

Many people think budgeting means giving up everything they enjoy, but that is not true. A realistic budget simply helps track income and expenses so spending stays under control. The key is creating a budget that fits real life rather than trying to follow impossible financial rules.

Start by listing monthly income and all regular expenses such as rent, food, transportation, bills, and entertainment. Once spending patterns become clear, it becomes easier to identify areas where money can be saved.

Build an Emergency Fund

Life is unpredictable. Medical emergencies, job loss, car repairs, or unexpected bills can happen at any time. An emergency fund acts as a financial safety net during difficult situations.

One of the smartest money moves is setting aside savings specifically for emergencies. Financial experts often recommend saving enough to cover three to six months of living expenses.

Building an emergency fund takes time, especially for people living paycheck to paycheck. However, even small savings matter. Saving a little each month consistently can eventually create financial stability.

Keeping emergency savings separate from everyday spending accounts also reduces the temptation to use the money unnecessarily.

Avoid Unnecessary Debt

One of the best financial habits is spending within personal limits. Before buying something expensive, it helps to ask whether the purchase is truly necessary or simply an impulse decision.

Debt can quickly become one of the biggest obstacles to financial growth. While some debt, such as home loans or education loans, may be useful in certain situations, high-interest debt can create long-term financial pressure.

Credit card debt is especially dangerous because interest rates are often very high. Many people fall into a cycle where they only make minimum payments while the balance continues growing.

One of the best financial habits is spending within personal limits. Before buying something expensive, it helps to ask whether the purchase is truly necessary or simply an impulse decision.

Start Investing Early

Investing is one of the most powerful ways to build wealth over the long term. Many people delay investing because they think they need large amounts of money to begin, but even small investments can grow significantly over time.

The earlier someone starts investing, the more time their money has to grow through compound returns. Compound growth means earnings begin generating additional earnings, creating long-term financial growth.

There are many investment options available, including stocks, mutual funds, retirement accounts, and index funds. Beginners often benefit from starting with simple and low-risk investment strategies before exploring more advanced options.

Consistency matters more than trying to become rich quickly. Regular investing over many years often produces better results than risky short-term decisions.

Track Spending Habits

Many people underestimate how much they spend on small daily purchases. Coffee, online shopping, food delivery, subscriptions, and impulse buying may seem harmless individually, but together they can consume a large part of monthly income.

Tracking expenses creates awareness. Once spending habits become visible, it becomes easier to make smarter financial decisions.

Using budgeting apps or simple spreadsheets can help monitor spending patterns. The goal is not to eliminate every enjoyable purchase but to make intentional decisions about money.

Understanding spending habits also helps identify emotional spending triggers. Some people spend more money when stressed, bored, or unhappy. Recognizing these patterns can improve both financial and emotional well-being.

Increase Financial Knowledge

Financial education is one of the best investments anyone can make. Unfortunately, many schools do not teach important topics such as budgeting, investing, taxes, or retirement planning.

Learning about personal finance helps people make informed decisions instead of relying on guesswork or bad advice. Reading books, listening to podcasts, watching educational videos, and following trusted financial experts can improve financial understanding.

The more knowledge people gain, the more confident they become when managing money. Financial literacy also reduces the chances of making costly mistakes.

Even basic financial knowledge can have a major impact on long-term financial health.

Save for Retirement Early

Retirement may seem far away for younger people, but starting early provides a huge advantage. Waiting too long often means needing to save much larger amounts later in life.

Retirement savings should become a regular financial habit, even if contributions start small. Many employers offer retirement plans that include matching contributions, which can significantly increase long-term savings.

The earlier retirement investing begins, the more time investments have to grow. Time is one of the biggest advantages in retirement planning.

People who start saving early often experience less financial pressure later in life and gain greater freedom when planning their future.

Diversify Income Sources

Relying on a single source of income can be risky. Losing a job or facing unexpected financial difficulties can create serious challenges.

One smart money move is developing additional income streams. Freelancing, online businesses, investments, rental income, or side projects can provide extra financial security.

Multiple income sources also create more opportunities for saving and investing. Many successful people build wealth not only through their main job but also through side income opportunities.

Technology has made it easier than ever to earn additional income online. Skills such as writing, graphic design, teaching, video editing, and digital marketing can all create new financial opportunities.

Protect Your Financial Future

Insurance is often overlooked, but it plays an important role in financial planning. Health insurance, life insurance, and property insurance can prevent financial disasters during unexpected situations.

Without proper protection, medical emergencies or accidents can destroy years of financial progress. Insurance helps reduce financial risk and provides peace of mind.

Another important step is protecting personal information and financial accounts from fraud. Strong passwords, secure banking habits, and monitoring financial statements regularly can help prevent identity theft and scams.

Financial security is not only about growing money but also protecting it.

Set Clear Financial Goals

Financial success becomes easier when people have clear goals. Without direction, it is easy to spend money without thinking about the future.

Goals may include buying a home, paying off debt, traveling, starting a business, or achieving financial independence. Clear goals provide motivation and help guide financial decisions.

Short-term and long-term goals both matter. Small goals create momentum and confidence, while larger goals encourage long-term planning.

Writing down financial goals and reviewing them regularly increases focus and accountability.

Learn the Difference Between Needs and Wants

One of the most valuable financial lessons is understanding the difference between needs and wants. Needs are essential expenses such as housing, food, healthcare, and transportation. Wants are optional purchases that improve comfort or entertainment.

Modern advertising constantly encourages people to spend more money. Social media also creates pressure to buy expensive products and lifestyles.

Learning to prioritize needs over unnecessary wants helps build financial discipline. This does not mean avoiding enjoyment completely. It simply means making thoughtful choices instead of emotional purchases.

Over time, disciplined spending creates more opportunities for saving, investing, and achieving important life goals.

FAQ’s

- What are personal finance money moves?

Smart habits to manage, save, and grow your money effectively. - Why is budgeting important?

It helps track spending and control financial decisions. - What is an emergency fund?

Savings kept for unexpected expenses or financial emergencies. - Why should I start investing early?

It allows your money to grow faster through compound interest. - How can I improve my finances?

By saving more, spending wisely, and avoiding unnecessary debt.

- Powerful Money Moves to Boost Savings and Grow Wealth

- Easy DIY Crafts to Make Your Space Look Beautiful

- Trend Crafting Secrets Every Creator and Brand Should Know

- 10 Powerful Books That Can Transform Your Thinking

- 7 Easy DIY Room Hacks That Made My Space Look Expensive

- The Biggest Obstacles to Personal Growth and How to Conquer Them

0 Comments